Understanding 401(k) Withdrawal Penalties: What You Need to Know

Keywords: 401(k) withdrawal penalty, early withdrawal, retirement savings, tax-advantaged retirement plans

Introduction

Planning for retirement is crucial, and many individuals rely on tax-advantaged retirement plans like 401(k)s to save for their future. However, unexpected circumstances may arise, and you may find yourself in need of accessing your retirement funds before reaching the age of 59 ½. While early withdrawals from 401(k) plans are possible, they often come with penalties and tax consequences. In this comprehensive guide, we will explore the rules and regulations surrounding 401(k) withdrawal penalties, exceptions to these penalties, and alternative options to consider when faced with financial difficulties.

Understanding 401(k) Withdrawal Penalties

What is a 401(k) Withdrawal Penalty?A 401(k) withdrawal penalty refers to the additional charges imposed by the Internal Revenue Service (IRS) when you withdraw funds from your 401(k) plan before reaching the age of 59 ½. These penalties are designed to discourage individuals from prematurely accessing their retirement savings and promote long-term participation in employer-sponsored retirement plans.

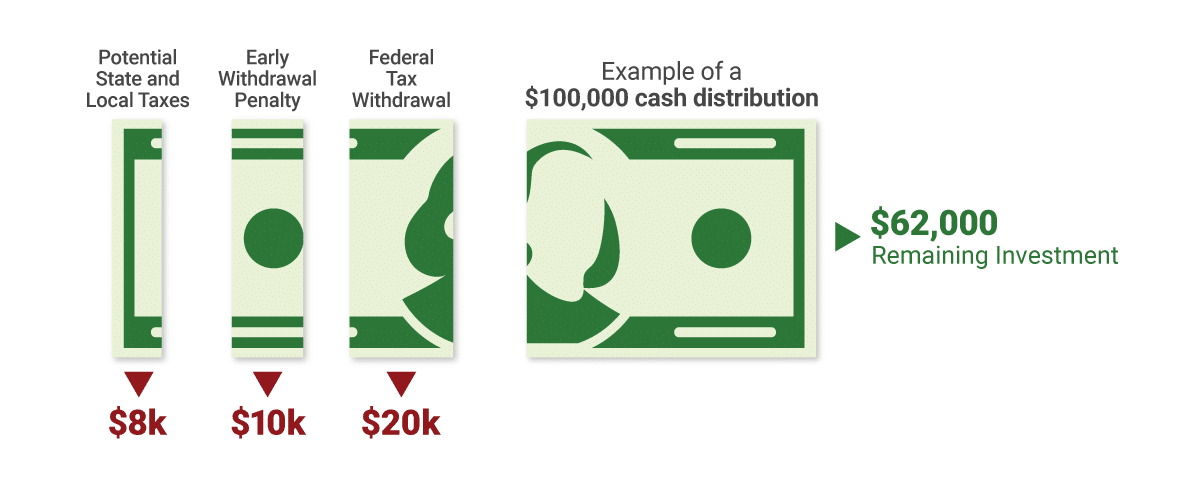

The Costs of Early 401(k) WithdrawalsEarly withdrawals from a 401(k) account can be expensive, as they typically incur federal income tax, a 10% penalty, and relevant state income tax. These financial implications can significantly impact your retirement savings and should be carefully considered before making any early withdrawals.

What to Ask Yourself Before Making a 401(k) WithdrawalBefore deciding to withdraw funds from your 401(k) plan, it is essential to evaluate your financial situation and consider the long-term consequences. Ask yourself if you genuinely need the money at this moment and explore alternative options to avoid tapping into your retirement savings. Building an emergency fund, utilizing promotional credit card offers, seeking help from friends and family, or considering a personal loan are some of the alternatives worth considering.

Exceptions to 401(k) Withdrawal Penalties

401(k) Hardship WithdrawalsCertain 401(k) plans allow for hardship withdrawals, which may exempt you from incurring the 10% penalty. However, it is important to note that the eligibility and qualifying expenses for hardship withdrawals vary depending on your specific 401(k) plan. While education expenses may fall under the hardship withdrawal clause for some plans, this is not universally applicable.

Medical Expenses or InsuranceIf you have incurred unreimbursed medical expenses that exceed a certain percentage of your adjusted gross income, you may be able to withdraw funds from your IRA or 401(k) without incurring the 10% penalty. The threshold for medical expense exemptions differs between IRAs and 401(k) plans, so it is important to familiarize yourself with the specific requirements.

Family CircumstancesIn certain situations where you are legally obligated to provide financial support to divorced spouses, children, or dependents, the IRS may waive the 10% penalty for early withdrawals from your retirement accounts.

Series of Substantially Equal PaymentsIf none of the aforementioned exceptions apply to your circumstances, you may consider taking a series of substantially equal payments from your IRA or 401(k) without incurring the 10% penalty. However, it is crucial to adhere to the IRS guidelines regarding the calculation of these payments and the duration for which they must be made.

Education ExpensesQualified higher education expenses, such as tuition, books, fees, and supplies, may qualify for penalty-free withdrawals from your IRA. However, it is important to note that these withdrawals will still be subject to income tax.

First-Time Home PurchaseIf you are a first-time homebuyer, you may be eligible to withdraw up to $10,000 from your IRA without incurring the 10% penalty. This exception also extends to your spouse, allowing both of you to utilize this benefit for a home purchase. However, it is important to meet the IRS definition of a first-time homebuyer and adhere to the specific requirements.

401(k) LoanIf your employer permits it, you may consider taking a loan from your 401(k) rather than making an early withdrawal. This option allows you to borrow against your 401(k) balance, with the interest paid back to yourself. While 401(k) loans can be a viable alternative, it is important to understand the terms and potential consequences, such as repayment requirements and the impact on your retirement savings.

Pros and Cons of 401(k) Withdrawals and Loans

401(k) WithdrawalsPros:

- No requirement to pay back the withdrawn amount

- Flexibility to access 401(k) assets

- No need for credit checks or impact on credit score

Cons:

- Incurs federal income tax and relevant state tax

- Subject to the 10% penalty

- Diminishes the potential for compounding and long-term growth

401(k) LoansPros:

- No taxes or penalties on loans

- Interest paid goes back into your retirement plan

- No impact on credit score

Cons:

- Repayment requirements, especially if you leave your current job

- Potential penalties if unable to repay the loan

- Opportunity cost of missed compounding and growth potential

Alternative Options to Consider

While early withdrawals and loans from your 401(k) may seem like immediate solutions to financial difficulties, it is important to explore alternative options before tapping into your retirement savings. Building an emergency fund, taking advantage of low-interest promotional credit card offers, seeking support from friends and family, or considering personal loans are potential alternatives that can help manage unexpected expenses without compromising your retirement savings.

Conclusion

Navigating the world of 401(k) withdrawals can be complex, and it is essential to understand the potential penalties, exceptions, and alternative options available to you. Before making any decisions, thoroughly assess your financial situation, consider the long-term implications, and explore alternative avenues for meeting your immediate needs. Remember, retirement savings are designed to support you in your golden years, and careful planning and decision-making can help ensure a secure financial future.